I'm excited. Guest post! Always wanted to do this.

FYI - any of you readers, if you want to put some thoughts up here, email me. You all know how to contact me.

This post is from Pramod Khargonekar.

Martin Wolf is a highly respected and influential economist who writes a regular column for Financial Times (

www.ft.com). A wonderful article, Call of the Wolf, describing on Martin Wolf can be found at

http://www.tnr.com/article/economy/call-the-wolf?page=0,0.

In his article in FT on September 15, 2009 (

http://www.ft.com/cms/s/0/b24477de-a226-11de-9caa-00144feabdc0.html), he wrote an excellent piece on what lessons we can take away from the fall of Lehman brothers a year ago.

“If the price of oil stabilises, I believe we can weather the financial crisis at limited cost in terms of real activity.” Thus did Olivier Blanchard, newly appointed head of the International Monetary Fund’s research department, describe the prospects ahead on September 2 2008. He was swiftly proved wrong

Few economists then realised how fragile the global financial system had become. The failure of Lehman Brothers just under two weeks later and the ensuing crisis at AIG, the insurance giant, turned complacency into terror. The financial system plunged into an abyss, dragging the economy behind it.

This is only partially true. People like Roubini, Schiff, and many others did warn of the troubles quite accurately. But the larger point that the collapse stunned most of the people is quite true.

What lessons are we to learn from this shock, a year later?

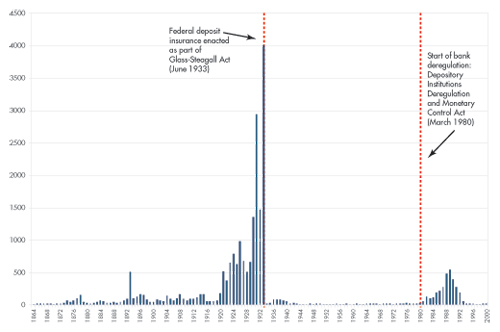

Above all, the true insurers of the financial system can be seen in our mirrors. According to the IMF’s Global Financial Stability Report of April 2009, total support for the financial system from the governments and central banks of the US, the eurozone and the UK has amounted to $8,955bn (£5,436bn, €6,132bn) – $1,950bn in liquidity support, $2,525n in asset purchases and $4,480bn in guarantees.

These numbers should be etched on a large stone on Wall and Broad Street. To put these numbers in perspective, US annual GDP is around $14,000bn. So, we have spent close to 60% of US annual GDP to support the companies in the financial sector.

These sums are misleadingly precise. The painful truth is that the incomes of taxpayers were put at the disposal of the financial sector’s creditors. When finance ministers and central bank governors of the Group of Seven leading developed countries met in Washington last October, they decided to “take decisive action and use all available tools to support systemically important financial institutions and prevent their failure”. Desperate times; desperate measures.

Since large financial institutions are most likely to fail during a crisis, this amounted to an open-ended government guarantee. What makes the decision quite unbearable is that it was, in my view, also correct. The risk of a cascading failure of the good, the bad and the ugly among financial institutions was apparent. Given what had happened after Lehman’s failure, only fools would have run this experiment. We were not that foolish.

This is the key argument --- the bailout was necessary. There is the other side of the argument which says we should let companies fail. It is impossible to know which would have been the better choice: bailout as was done or let them fail. At this point, it is an academic issue. Indeed, what has been done to deal with this crisis will be used to draw lessons when it comes to future crises which are bound to happen. In this sense, Ben Bernanke, Hank Paulson, Tim Geither, Larry Summers are writing the book which will be studied by future economists and policy makers.

Thus, the lesson learnt from Lehman’s failure was the precise opposite of what many had hoped on the day it was announced: it is that every systemically significant institution must be rescued in a crisis. That lesson is reinforced by Wednesday’s agreement that the rescue, buttressed by unprecedented monetary and fiscal stimulus, has worked: the panic is over and the world economy is on the mend.

We still have so many systemically important institutions. So, there has been no change in the “too big to fail” situation.

Indeed, one can argue that the Lehman failure was necessary. Without such an event, there was no chance of obtaining the resources needed to resolve the crisis, above all from the US Congress. This is what the Harvard historian Niall Ferguson argued in the FT on Tuesday. It is likely that he is right.

Everything, in short, has been for the best in the best of all possible worlds. In retrospect, it was right to let Lehman go, because it caused such a disaster. That then forced a public sector resolution of the crisis and taught that such a failure must never be allowed again. If these are indeed the sorts of lessons we draw, we are making huge mistakes.

We are now getting to the punch lines of the Wolf article:

First, we cannot let stand the doctrine that systemically significant institutions are too big or interconnected to be allowed to fail in a crisis. No normal profit-seeking business can operate without a credible threat of bankruptcy.

Thus, President Barack Obama is correct to call for the “most ambitious overhaul of the financial system since the Great Depression”. The communiqué of the Group of 20 finance ministers and central bank governors outlines the current agenda for reform. It is quite sensible, so far as it goes.

The question, however, remains whether enough will be done to eliminate the present incentives to game the system. It must be possible to wind up institutions without the damage we witnessed after Lehman’s collapse. This has come to be called a “living will”. A better term would be “assisted euthanasia”. Should that be impossible, these institutions must be under the sort of regulation that we normally apply to utilities.

I have previously talked about the “public utility” model for the financial sector. (

ed. note: I summarized some of his thoughts on this idea in this post.) It is great to see that Wolf also advocates the same notion. The only other way is to have a well designed system that eliminates the very notion of too big to fail.

The second big potential mistake is to return to the old doctrine that it is better to clean up after a crisis than to take any pre-emptive action. Yet, the more effective the present clean-up seems, the more likely is it that central bankers will draw that lesson. They can argue that, if we have been able to survive such a huge crisis, no changes in the policy orthodoxy are needed.

This would be a huge error, as William White, formerly chief economist of the Bank for International Settlements, argues in a thought-provoking paper.* Mr White, one of the few economists in the official sector to warn of a looming crisis, argues that the “macroprudential” approach, now increasingly accepted, cannot rely on regulation alone. It is almost impossible for such regulation to offset the powerful incentives for credit creation produced by expansionary monetary policies. Thus, argues Mr White, “pre-emptive tightening” should replace “pre-emptive easing”. If we look back at the past two decades of ever more desperate efforts to clean up after crises, the wisdom of this “belt and braces” approach will seem evident.

I think it is an interesting intellectual problem. Can one design a system to detect bubbles? Can one create numerical measures of “bubbliness”? It sounds like an engineering or machine learning problem. It may be hard, possibly impossible, since the system may change over time making the measures designed on the basis of past data inadequate or useless.

(ed. note: a commentor on this blog has argued against the idea of preemptive bubble killing in the comments in this post.)The third big mistake is more immediate: it is to assume that we are already well on the way to a healthy recovery. The financial panic is indeed over, as it should be, given the scale of government guarantees. The economic dangers are not.

The recovery has been fuelled by the bail-out of the financial system and by extraordinary fiscal and monetary policies, particularly in the countries with the highest private-sector leverage. For good reason, the private sectors of such countries are likely to save more and pay down debt for years to come. This, in turn, now necessitates a big swing in the balance between supply and demand in export-dependent economies.

Mr Blanchard has set out the post-crisis macroeconomic agenda in a recent article.** As he puts it, we must manage delicate “rebalancing acts” – first, “rebalancing from public to private spending”; second, “rebalancing aggregate demand across countries”. Unless and until both are managed, the recovery is built on quicksand.

Only the future will tell whether the recovery is sustainable or built on quicksand. It is amazing how the stock market anticipated the current recovery. As it happens, real economy responds to perceptions of people (which in turn are influenced by the stock market and jobs and the real economic conditions. (Soros calls this reflexivity. It is also related to the idea of animal spirits, currently championed by Akerloff and Shiller.)

Letting Lehman go was not our biggest mistake. That was letting the economy and financial system become so vulnerable. Equally, the past year has restored neither the financial system nor the economy to health. We have avoided the worst. That is good. It is not enough.

There it is. A multi trillion dollar question is: will we really make any substantial changes in response to this major collapse which has led to near 10% unemployment rate!

{kind=link}